The GENIUS Act — U.S. Legal Recognition of Stablecoin Settlement

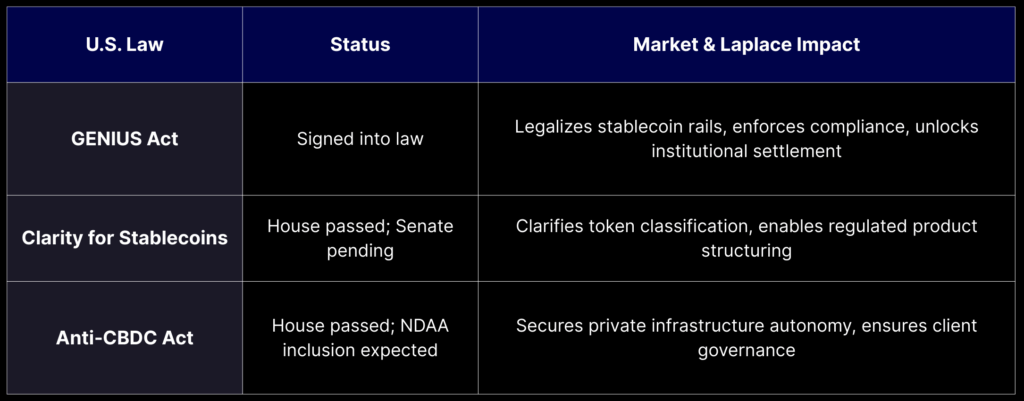

Signed into law on July 18, 2025 with bipartisan support, the GENIUS Act (S.1582) establishes the first federal stablecoin framework. It mandates one-to-one reserve backing, redemption rights, monthly public disclosures, and titles issuers as Registered Permitted Payment Stablecoin Issuers (PPSIs). The Act also defines a clear compliance timeline: regulations become effective either within 120 days of rulemaking or by January 18, 2027, with a safe harbor for legacy stablecoins and prioritized claims in bankruptcy proceedings.

This legislation converts stablecoins from a regulatory gray area into a recognized, auditable settlement rail. Laplace is uniquely positioned to integrate U.S. compliant stablecoin issuers into our product infrastructure, enabling institutional clients to fund and redeem through mechanisms grounded in U.S. law. This clarity removes operational friction, accelerates settlement, and enhances institutional trust in on-chain transactions.

Strategic Impact for Laplace

While Laplace is not yet a legacy institution with hundreds of deals or billions under management, that is precisely what positions us to lead. We’ve built our infrastructure from the ground up for a post-regulatory-clarity era without legacy dependencies, legacy cost structures, or outdated product logic. Our business model is designed to scale with the needs of mid-market institutions and sophisticated investors that are traditionally underserved, offering them access to institutional-grade, tokenized investment opportunities with the same transparency and governance standards demanded by the world’s top allocators.

As these U.S. laws reshape global standards, it’s not just the size of the institution that matters. It’s whether the architecture is aligned with the future.

Overall, these laws combine to shape a cohesive regulatory ecosystem perfectly aligned with Laplace’s compliant infrastructure under the regulated authority of MAS, for global institutions and investors:

- Settlement Certainty

The GENIUS Act transforms stablecoins into U.S.-recognized settlement rails, enabling institutions to engage in tokenized investment without exposure to legal or operational uncertainty. - Product Governance Clarity

The Clarity Act removes classification risk across token lifecycles, allowing Laplace to design and distribute structured investment instruments with legal visibility from issuance to maturity. - Institutional Infrastructure Sovereignty

The Anti‑CBDC Act ensures that private, auditable platforms—not government-led alternatives—remain centerstage in financial innovation, preserving client control and institutional governance norms. - Global Regulatory Alignment

Coupled with Singapore’s MAS-regulated environment, these U.S. laws position Laplace at the intersection of two of the most advanced global compliance systems, enabling seamless execution, distribution, and regulatory alignment across continents.

This confluence significantly reduces the risk premium that once deterred institutional allocations into tokenized markets. Laplace is not only compliant with these frameworks – it was designed for us, in order to shape the financial world to better serve the gap of unrealized institutions and investors.

Summary Table